APR Distorts Flat Fee for Short-Term, Small-Dollar Loans

What a Short-Term, Small-Dollar Loan Really Costs

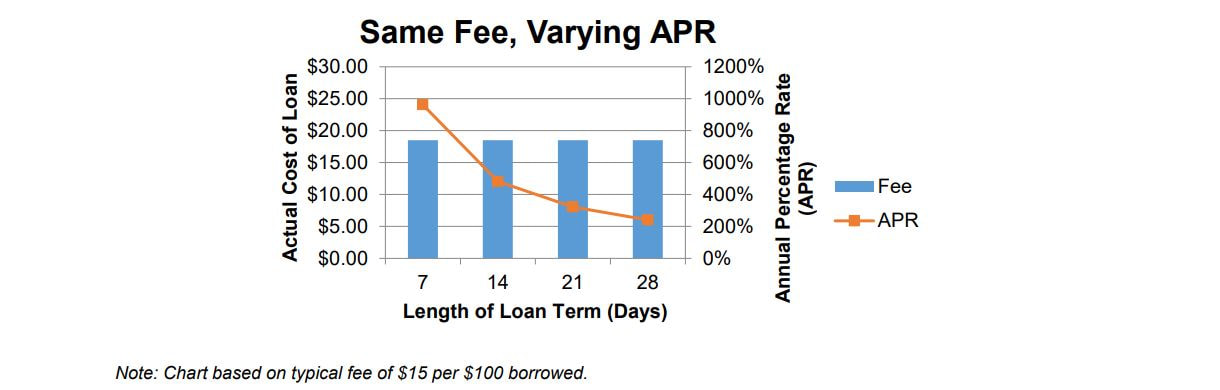

There’s a lot of confusion about what a short-term, small-dollar loan costs, but customers would tell you that the answer is simple and straightforward: typically, $15 to borrow $100 until your next payday. Period.

There are no hidden fees, no compounding interest – just $15. Whether a customer repays their loan in three days or 30, they will pay the same one-time fee.

Annual Percentage Rate (APR): A Flawed Calculation

As required by the Truth in Lending Act (TILA), consumer credit providers always disclose the fee associated with services as both a dollar amount and an APR. But, due to the short-term nature of the loan, APR is not an appropriate value indicator.

The APR calculation disclosed by lenders represents the implied annual rate for a short-term, small-dollar loan, and assumes that a small-dollar loan is extended 26 times – or every two weeks – during a year, with the customer paying a new fee each time. This is a flawed assumption. Customers use this service for a relatively short period of time – weeks or months. Disclosing APR on a short-term loan would be equivalent to a grocery store displaying the price of hamburger meat by the ton, or if a parking meter listed the rate for a year’s worth of parking.

______________________________________________________________________________________________________________________

$15 Typical Loan Fee (per $100 Borrowed) x 26 # of Consecutive 14-day Cycles = 391% Implied APR

______________________________________________________________________________________________________________________

There’s a lot of confusion about what a short-term, small-dollar loan costs, but customers would tell you that the answer is simple and straightforward: typically, $15 to borrow $100 until your next payday. Period.

There are no hidden fees, no compounding interest – just $15. Whether a customer repays their loan in three days or 30, they will pay the same one-time fee.

Annual Percentage Rate (APR): A Flawed Calculation

As required by the Truth in Lending Act (TILA), consumer credit providers always disclose the fee associated with services as both a dollar amount and an APR. But, due to the short-term nature of the loan, APR is not an appropriate value indicator.

The APR calculation disclosed by lenders represents the implied annual rate for a short-term, small-dollar loan, and assumes that a small-dollar loan is extended 26 times – or every two weeks – during a year, with the customer paying a new fee each time. This is a flawed assumption. Customers use this service for a relatively short period of time – weeks or months. Disclosing APR on a short-term loan would be equivalent to a grocery store displaying the price of hamburger meat by the ton, or if a parking meter listed the rate for a year’s worth of parking.

______________________________________________________________________________________________________________________

$15 Typical Loan Fee (per $100 Borrowed) x 26 # of Consecutive 14-day Cycles = 391% Implied APR

______________________________________________________________________________________________________________________

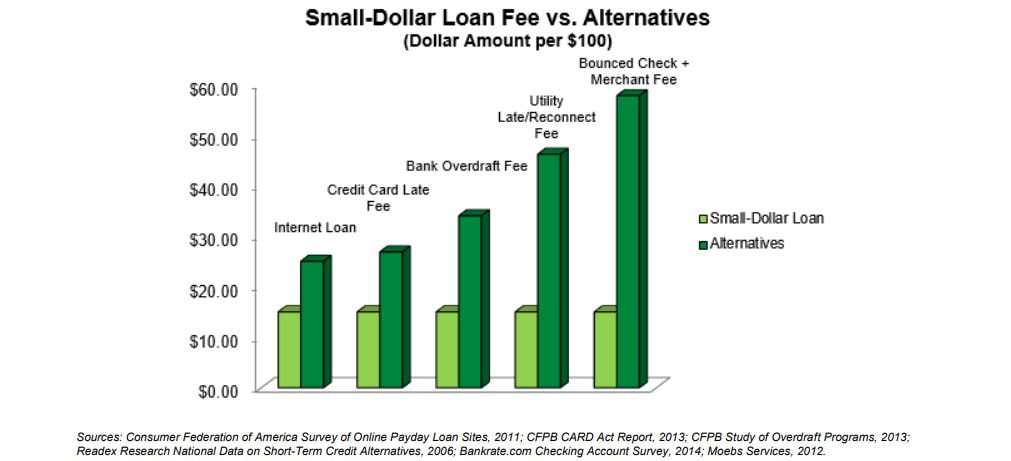

The Alternatives

A short-term, small-dollar loan’s one-time fee often proves to be less expensive than the costs associated with other alternatives – including unregulated Internet loans, overdraft usage, bounced checks, late payments to credit card companies and utility reconnections.

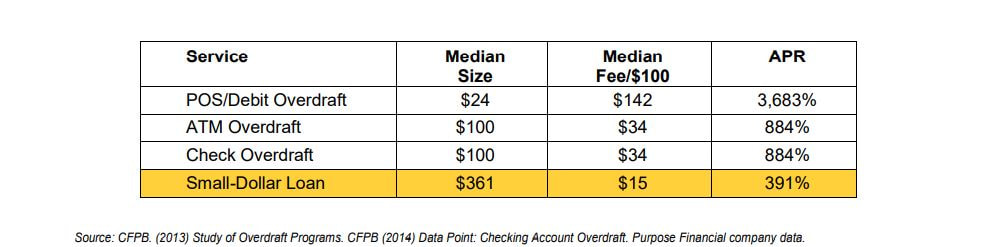

Short-term, small-dollar loans are often the most cost-effective option even when comparing the implied APR for a loan against the annual rates of bank overdraft programs. Unlike short-term, small-dollar loans, the services below are not required by law to publish the fee as an APR.

Even federal regulators and bank and credit union officials have said that APR is not an accurate measurement for short-term, small-dollar credit.

______________________________________________________________________________________________________________________

“Any time an annual percentage rate is calculated for a term less than a year, the inclusion of a fixed fee, even a modest one, will distort and overstate the APR. The shorter the repayment period, the greater the APR will appear in instances where there is a fixed fee. This means that the sooner the consumer repays, the greater the calculated APR – a difficult concept to explain to consumers, as it appears that paying earlier actually increases the cost of credit.”

– Kenneth J. Clayton, American Bankers Association (ABA)

______________________________________________________________________________________________________________________

Eliminating Credit through APR Caps

Despite these facts, a number of state legislatures have pursued misguided legislation that would impose an APR cap on small-dollar loans – amounting to an effective ban. In fact, the Center for Responsible Lending, which has led the campaign to prohibit small-dollar lending in various states, said that one state’s policymakers “fully understood that [an APR cap] would ban the product,” when the legislature passed an APR cap in 2008.1

Several states and the District of Columbia have implemented APR caps, including Arkansas, Arizona, New Hampshire, Ohio and Oregon. These actions created an environment that was not economically viable for many lenders, as they were unable to cover basic operating costs, such as wages, rent and utilities.

For example:

• Under a 36 percent APR cap, a $100 loan would yield a $1.38 fee. No business – not a credit union, not a bank – can sustainably lend money to many customers for less than 10 cents a day without being subsidized.

• Lenders in these states were forced to close hundreds of centers, costing thousands of employees their jobs and leaving consumers with fewer credit options.

• Historically, price fixing of any kind almost always results in reduced consumer access to any product.

Interest rate caps harm consumers by eliminating a critical choice for thousands of people who need short-term, small-dollar credit, forcing them to choose costlier or less regulated options, such as overdraft loans or illegal loans. 1 Business TN, September 2008.

______________________________________________________________________________________________________________________

“Any time an annual percentage rate is calculated for a term less than a year, the inclusion of a fixed fee, even a modest one, will distort and overstate the APR. The shorter the repayment period, the greater the APR will appear in instances where there is a fixed fee. This means that the sooner the consumer repays, the greater the calculated APR – a difficult concept to explain to consumers, as it appears that paying earlier actually increases the cost of credit.”

– Kenneth J. Clayton, American Bankers Association (ABA)

______________________________________________________________________________________________________________________

Eliminating Credit through APR Caps

Despite these facts, a number of state legislatures have pursued misguided legislation that would impose an APR cap on small-dollar loans – amounting to an effective ban. In fact, the Center for Responsible Lending, which has led the campaign to prohibit small-dollar lending in various states, said that one state’s policymakers “fully understood that [an APR cap] would ban the product,” when the legislature passed an APR cap in 2008.1

Several states and the District of Columbia have implemented APR caps, including Arkansas, Arizona, New Hampshire, Ohio and Oregon. These actions created an environment that was not economically viable for many lenders, as they were unable to cover basic operating costs, such as wages, rent and utilities.

For example:

• Under a 36 percent APR cap, a $100 loan would yield a $1.38 fee. No business – not a credit union, not a bank – can sustainably lend money to many customers for less than 10 cents a day without being subsidized.

• Lenders in these states were forced to close hundreds of centers, costing thousands of employees their jobs and leaving consumers with fewer credit options.

• Historically, price fixing of any kind almost always results in reduced consumer access to any product.

Interest rate caps harm consumers by eliminating a critical choice for thousands of people who need short-term, small-dollar credit, forcing them to choose costlier or less regulated options, such as overdraft loans or illegal loans. 1 Business TN, September 2008.

|

CFSP is a proud member of INFiN

RESEARCH PROVIDED BY INFiN

|