Dispelling Common Myths: The Facts about Short-Term, Small-Dollar Loans

The realities of small-dollar loans are vastly different than the myths spread by industry critics. The following is a straightforward examination to help separate fact from fiction.

Myth #1: Short-term, small-dollar loans have unreasonably high interest rates.

FACT: Annual Percentage Rate is not an appropriate measure of the costs associated with short-term, small-dollar loans or the value they provide.

• The Federal Truth in Lending Act (TILA) requires all financial institutions to disclose loan fees as Annual Percentage Rates (APR). In order to comply with TILA, consumer financial services providers report the implied APR of their loans – the amount borrowers would pay in fees if they renewed their loan every two weeks for a full year.

• APR is not an appropriate measure of the costs associated with loans that last for less than a year, but rather is more accurate for long-term loans such as a mortgage or a car loan. The average short-term, small-dollar loan is only two to four weeks, while the typical small-dollar installment loan repayment will take anywhere from three to 36 months, depending on state regulations.

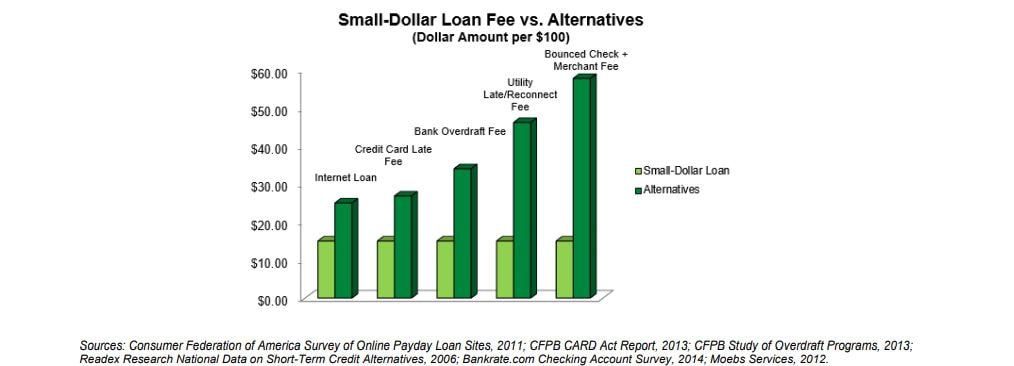

• When borrowing a small-dollar loan, consumers pay a set price for a short-term, small-dollar transaction. Customers appreciate that a short-term, small-dollar loan with a single payment comes with a one-time fee, which can be less expensive than the costs of bouncing a check, missing a credit card payment or neglecting a bill.

• The APR on a small-dollar loan decreases as the term lengthens; a small-dollar installment loan has a smaller implied APR than a two-week, small-dollar loan.

• Consumers choose these credit products because they are straightforward, transparent and often less costly than the alternatives. Whether comparing the direct cost or the APR of various options, consumers find that short-term, small-dollar loans provided by non-bank consumer financial services providers are still the least costly option compared to bank overdraft fees and bounced checks.

Myth #1: Short-term, small-dollar loans have unreasonably high interest rates.

FACT: Annual Percentage Rate is not an appropriate measure of the costs associated with short-term, small-dollar loans or the value they provide.

• The Federal Truth in Lending Act (TILA) requires all financial institutions to disclose loan fees as Annual Percentage Rates (APR). In order to comply with TILA, consumer financial services providers report the implied APR of their loans – the amount borrowers would pay in fees if they renewed their loan every two weeks for a full year.

• APR is not an appropriate measure of the costs associated with loans that last for less than a year, but rather is more accurate for long-term loans such as a mortgage or a car loan. The average short-term, small-dollar loan is only two to four weeks, while the typical small-dollar installment loan repayment will take anywhere from three to 36 months, depending on state regulations.

• When borrowing a small-dollar loan, consumers pay a set price for a short-term, small-dollar transaction. Customers appreciate that a short-term, small-dollar loan with a single payment comes with a one-time fee, which can be less expensive than the costs of bouncing a check, missing a credit card payment or neglecting a bill.

• The APR on a small-dollar loan decreases as the term lengthens; a small-dollar installment loan has a smaller implied APR than a two-week, small-dollar loan.

• Consumers choose these credit products because they are straightforward, transparent and often less costly than the alternatives. Whether comparing the direct cost or the APR of various options, consumers find that short-term, small-dollar loans provided by non-bank consumer financial services providers are still the least costly option compared to bank overdraft fees and bounced checks.

Myth #2: Small-dollar lenders could still operate profitably if they charged a much smaller APR.

FACT: Some industry critics have proposed capping interest rates for small-dollar lending services, but to do so would effectively ban short-term, small-dollar loans.

• Lower fees would not generate enough income to pay for basic business expenses, such as rent, utilities and wages.

• An APR of 36 percent on a two-week, small-dollar loan, as some industry critics have suggested, would mean customers pay a fee of $1.38 per $100 borrowed, or less than 10 cents per day.

• No market-based provider – not a credit union, not a bank – can sustainably lend a short-term, small-dollar loan at that rate without being subsidized. Such rate cap models overlook the significant cost of operating a regulated business, and would be an effective ban on small-dollar loans.

• Customers recognize that the price of the one-time fee is appropriate for a short-term, small-dollar loan, relative to other options.

• After South Dakotans passed a ballot initiative in 2016 that used a 36 percent rate cap to effectively eliminate the state’s regulated small-dollar lending industry, a little over a year later, reports found that most small-dollar lenders did not renew their licenses; only a few dozen licensed lenders remained. Credit counselors in the state suspect borrowers simply migrated to online lenders, while pawn shops reported a rise in business.

• One year after Oregon implemented a 36 percent interest rate cap, 75 percent of Oregon’s 360 small-dollar lending stores closed their centers. Consumer complaints against unregulated Internet lenders doubled, and nearly 70 percent of such complaints filed in 2010 were against unregulated online lenders.

• While some lenders claim to be able to operate under a 36 percent APR, the reality is that these providers serve a very different customer than the lenders that would be forced out of the market by a rate cap, typically only serving subprime customers – those with credit scores between 610 and 640 – whereas the average credit score for a person in need of non-bank credit is 579.

• Further, while these lenders may technically offer loans for 36 percent or less to a limited pool of subprime consumers, they often seek to evade this rate cap by offering expensive and unnecessary insurance products to their customers – services that are often implicitly positioned in loan agreements as required in order to qualify for the loan, and are not included in the loan’s APR calculation.

--------------------------------------------------------------------------------------------------------------------------------------------

“…a 36 percent cap eliminates payday loans altogether. If payday lenders earn normal profits when they charge $15 per $100 per two weeks, as the evidence suggests, they must surely lose money at $1.38 per $100 (equivalent to a 36 percent APR.)”

– Economists Robert DeYoung, Ronald Mann, Donald Morgan, and Michael Strain,

Federal Reserve Bank of New York

--------------------------------------------------------------------------------------------------------------------------------------------

Myth #3: Small-dollar loan customers should just go to a bank instead.

FACT: Consumers benefit from broad access to competitive credit options across principal amounts, terms, and providers, including regulated non-bank lenders.

• Most banks do not provide the kind of short-term, small-dollar loans that consumers need. The average amount of a small-dollar loan is about $370, significantly lower than what most banks will loan.

• Some banks and credit unions offer products they promote as “alternatives” but these options are not broadly available and involve a variety of restrictions and complex fee structures. In fact, a report by Professor Victor Stango “…a 36 percent cap eliminates payday loans altogether. If payday lenders earn normal profits when they charge $15 per $100 per two weeks, as the evidence suggests, they must surely lose money at $1.38 per $100 (equivalent to a 36 percent APR.)” – Economists Robert DeYoung, Ronald Mann, Donald Morgan, and Michael Strain, Federal Reserve Bank of New York of the University of California, Davis found that credit unions cannot viably serve as providers of small-dollar credit for customers currently served by small-dollar lenders.

• The few credit unions that offer comparable products charge fees and interest similar to those charged by retail lenders, but employ tighter credit requirements. Further, many consumers prefer non-bank lenders for reasons other than price, such as convenience.

• The federal banking regulators and the National Credit Union Administration are both exploring ways to encourage more banks and credit unions to offer small-dollar loans.

• CFSP supports a competitive market and encourages borrowers to weigh all of their options before choosing a small-dollar loan. Small-dollar loans are not for everyone, but customers make informed decisions, and choose these loans for their simplicity and reliability. • The Federal Reserve Bank of New York reports that access to credit choices contributes to individual and community credit health, economic mobility, and resiliency. • An array of credit options from different providers helps to eliminate the gaps that currently leave less-prime borrowers with few choices, resulting in greater parity in the credit marketplace so that all Americans can build credit.

Myth #4: Small-dollar lenders intentionally trap borrowers in a “cycle of debt.”

FACT: Consumers experiencing periodic financial challenges use small-dollar lending services as long as they need to – and only as long as they need to.

• Consumer financial services providers make loans that match, but do not exceed, customers’ needs. It hurts the company, and the customer, when a loan is not repaid.

• If a customer is unable to pay back a loan within the arranged timeframe, providers work with them to find the best way to deal with their individual situation.

• Regulated providers typically offer an Extended Payment Plan (where permitted under state law) that allows customers a longer time period to repay at no additional charge.

• According to research from credit reporting agency Clarity Services, “consumers who roll over small-dollar loans rather than paying them off are doing so because they choose to rather than being unable to,” effectively creating a “cycle of preference.” After considering credit score, monthly income (net and residual) and the availability of another credit line, Clarity’s research found that many consumers still choose to roll over a loan rather than pay it off, even though they might be financially able to do so.

Myth #5: Small-dollar lenders prey on unsophisticated customers.

FACT: Small-dollar loan borrowers are hardworking, middle-income consumers who understand and appreciate the simplicity, transparency and cost-effectiveness of this credit option.

• Small-dollar credit customers know precisely what they are getting and what it is costing them. They carefully weigh their options before borrowing a small-dollar loan, and choose the financial service that will help them overcome their challenges most effectively.

• According to a survey by Global Strategy Group (D) and Tarrance Group (R), 94 percent of borrowers agree that payday loans can be a sensible decision when consumers face unexpected costs, and 96 percent say they fully understood how long it would take to pay off their loan. Sixty-six percent of borrowers want to preserve their current ability to access payday loans.

• Additionally, the vast majority of borrowers say their lender clearly explained the terms of the loan (93 percent) and what would happen if the loan was not paid back in time (85 percent).

• Small-dollar credit customers are hardworking individuals – including small-business owners, teachers, nurses, bus drivers and first responders – who make positive contributions to their communities.

• All customers must have a steady source of income in order to receive a loan, and must have a checking account.

Myth #6: Small-dollar lenders offer loans without confirming a borrower’s ability to repay the loan.

FACT: Consumer financial services providers evaluate each and every customer’s ability to repay his or her own loan using an underwriting process.

• Regulated non-bank providers do not authorize loans that are more than a customer can afford to repay; that makes little business sense.

• Consumer financial services providers typically assess potential borrowers based on dozens of different factors including income, past credit performance, and eligibility under all applicable state and federal laws.

• Providers are committed to ensuring their customers are successful borrowers, and if a customer is unable to pay back their loan within the arranged timeframe, lenders will work with them to find the best way to deal with their individual situation and repay the loan.

|

CFSP is a proud member of INFiN

RESEARCH PROVIDED BY INFiN

|